Manganese ore prices in China beat market expectations: what drives the growth?

Impact of Collapsing Shipments to India on Manganese Market Outlook

28 July 2022Transnet Rail: No Changes to Existent Manganese Ore Railing Allocations

2 March 2023

The seaborne manganese ore prices witnessed another week of gains in China this week. The latest price developments seemingly ignore the portside stocks returning above 7 million tonnes and the country's obscure outlook amid a surge in covid outbreaks-affected areas. The current price trend in semicarbonate and high-grade market segments defies the long-term seasonal trend and might seem counterintuitive in light of the latest market sentiment.

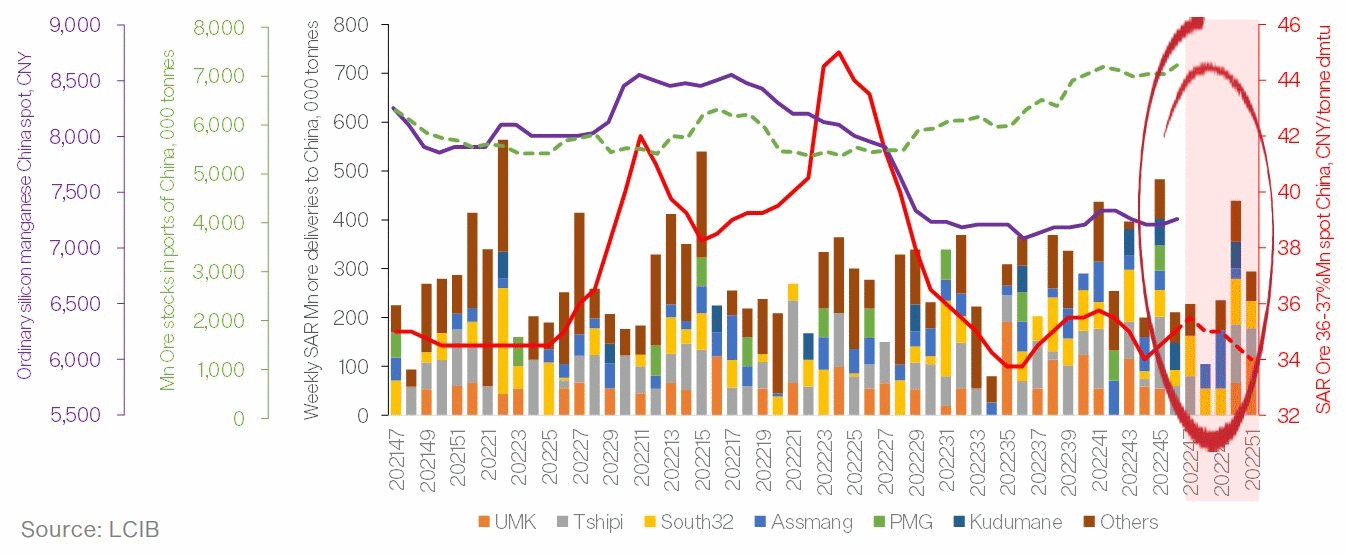

The deviations in price trend started with the recent growth in semicarbonate ore spot prices. As per LCIB forecast, the price upside was a result of South Africa's Transnet workers' strike action caused disruptions in early October. However, abundant semicarbonate inventories in China prevented China's market from factoring in the disruption immediately into the price at the time the strike occurred. Nonetheless, declining semicarbonate ore deliveries coupled with buoyant SiMn production amid improving recent steelmaking forced China spot 37%Mn SAR ore spot prices to return to growth on week 45.

Furthermore, recovering spot market consumption and insufficient volume on board in transit to China spurred gains in seaborne benchmarks.

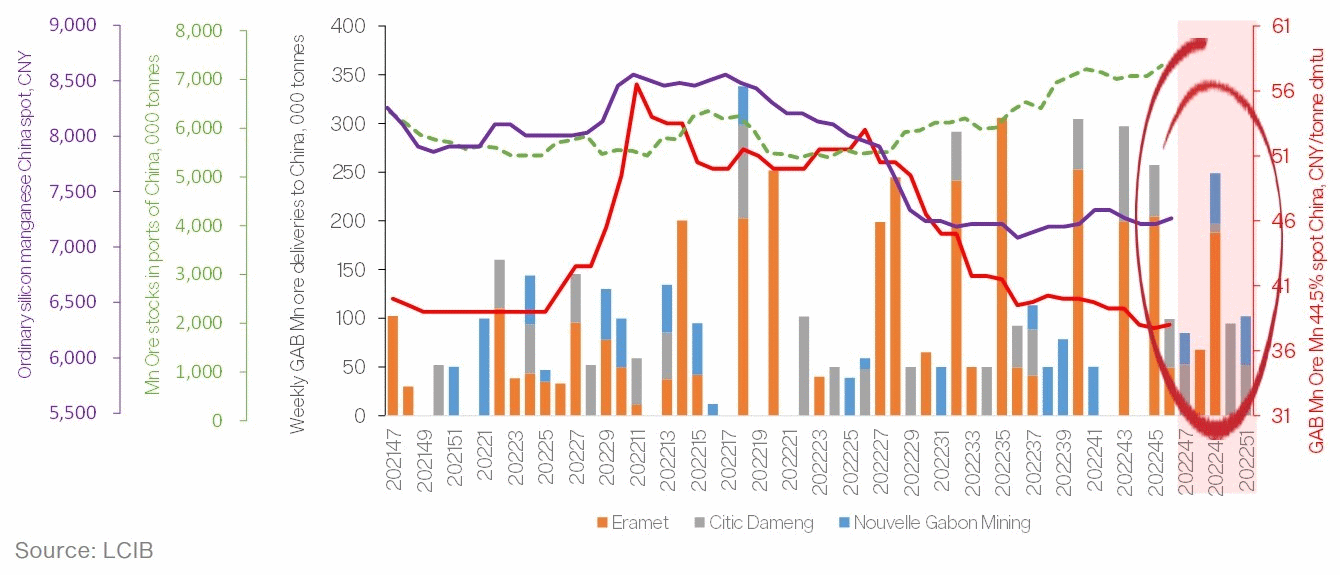

In addition, the change in the high-grade ore major suppliers' market positioning strategy makes the situation even more peculiar. #LCIB understands that after significantly ramping up production and sales, Gabon's Eramet has shifted its focus from taking over the market share from South32 due to the latter's decline in production towards further expanding its market share in China into the semicarbonate market segment. For instance, we heard that Gabon's miner had entered a long-term offtake agreement with Glencore as part of this strategic endeavour. Yet, despite a hike in Eramet's shipments, the company's actual deliveries to China remain fragmented (see Chart 1 below), leaving other sellers the window of opportunity in the event of a surge in Mn ore demand. This is what the market witnesses at the moment.

An improving immediate demand allowed other major high-grade ore supplier, Australia's South32, to bolster their seaborne prices this week, even despite a disappointing demand from FeMn producers recently.

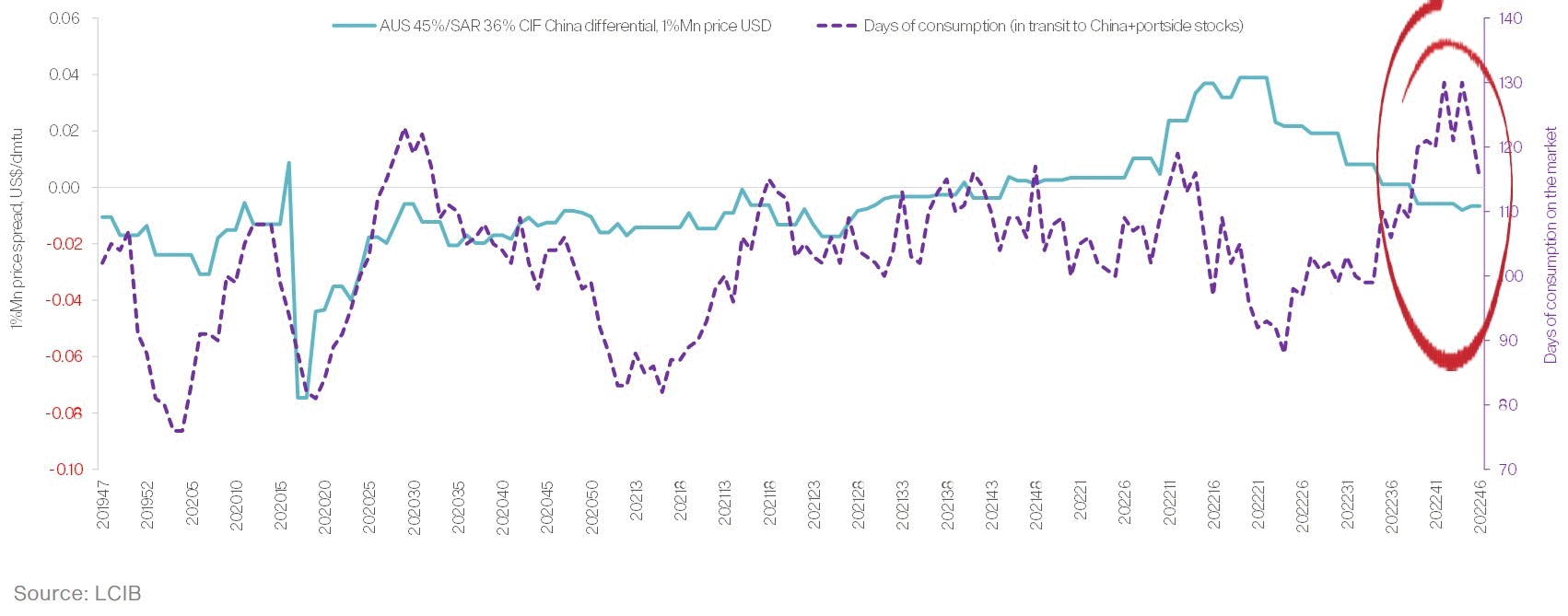

The price increase was expected amid a dramatic drop in Mn ore volume in transit to China, expressed as the days of consumption (see Chart 2) and was forecasted in the latest LCIB Manganese Market weekly report.

We expect the current upside to remain the subject of a) restricted imports of semicarbonate from South Africa to China in the nearest term (see Chart 3), b) the limited duration of crude steelmaking exceeding the long-term seasonal trend, which is likely to be shortlived despite piling up measures from the central government to support the economy, c) epidemiologic situation in the country.

{kind=link}

{kind=link}

{kind=link}