Impact of Collapsing Shipments to India on Manganese Market Outlook

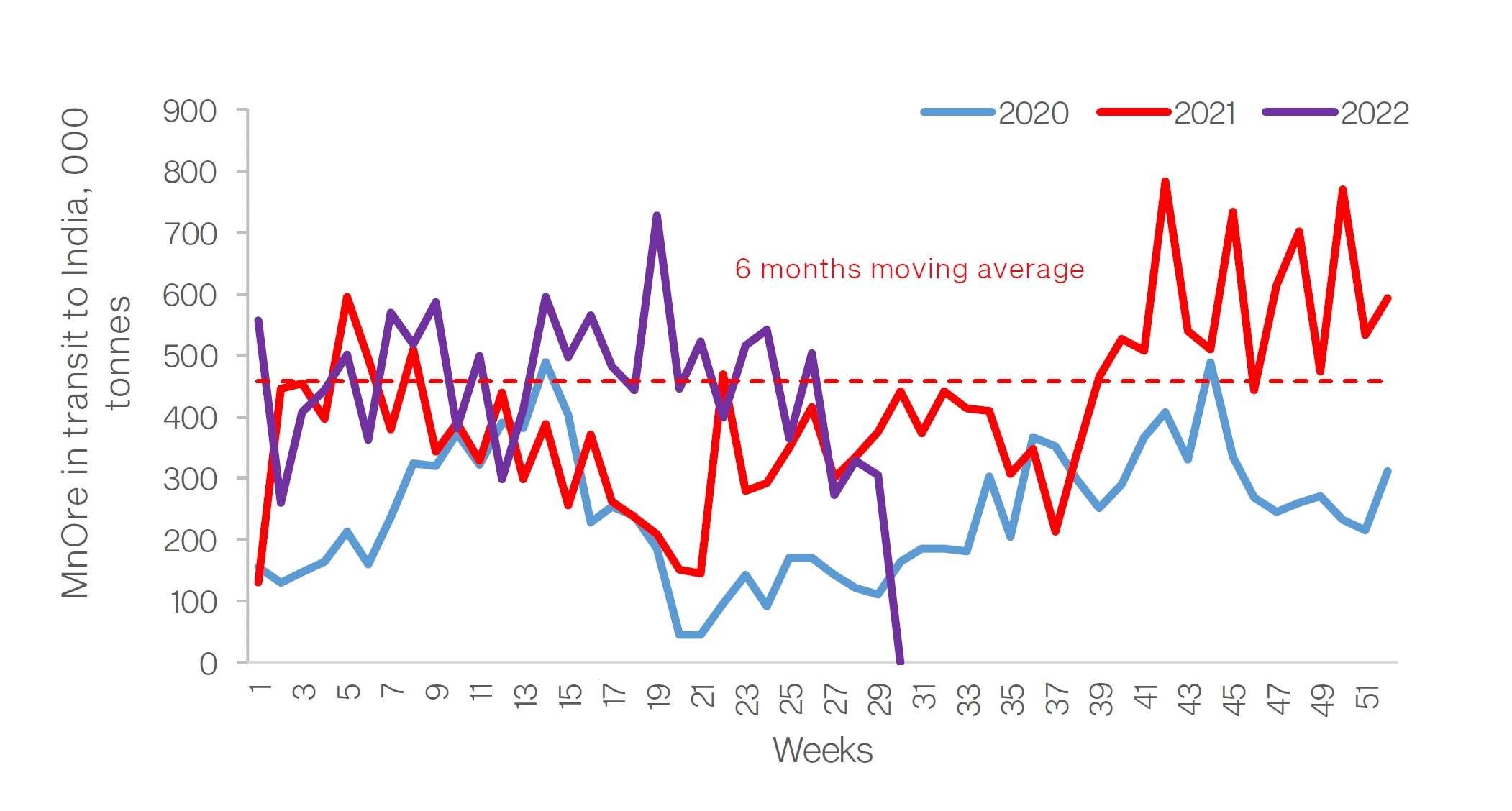

During H1 2022, India became the fastest-growing Mn Ore regional market

18 July 2022

Manganese ore prices in China beat market expectations: what drives the growth?

25 November 2022

The latest LCIB collected manganese ore shipment data indicates a sharp drop in exports to India. This, in turn, raises concerns that the absence of sales to India will inevitably translate into additional volumes being reverted to China. In the meantime, buoyant dispatches supported a steady growth of volumes in transit to China.

Despite being dampened by the recent decline in crude steel output amid slower-than-expected economic recovery, the slump can be, to an extent, attributed to seasonal factors on top of flawed fundamentals. For instance, seaborne Mn ore restocking precedes a seasonal pick-up in steel production in China and is typically observed in August. The current market observations suggest manganese demand evolution in China within the next 2-4 weeks will become the critical factor defining the price levels for the rest of the year, possibly until March 2023.

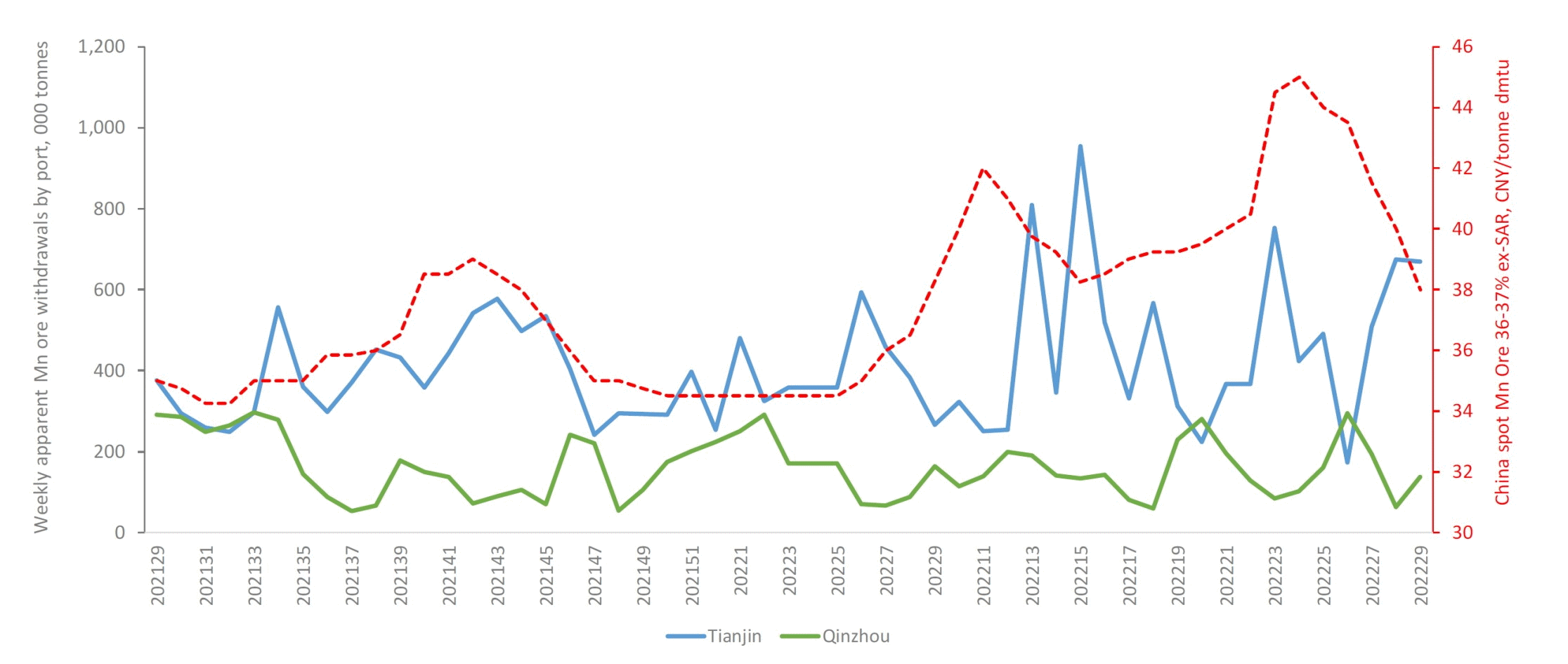

Fundamentally, the current consensus assumes that we will witness a rebound in steelmaking during Q3 and Q4 2022, which will, in turn, propel the demand for Mn ore. However, in light of the prospects of frail recovery rates of steelmaking in China, the market is facing a growing probability that there will be no clear restart of buying on the seaborne market due to overhanging Mn ore stocks already in China. In addition, despite negative price dynamics, LCIB shipment tracking data suggests that nine-month high shipments took place on week 29, ignoring the deteriorating prices. At the same time, data collected suggest consistently high Mn ore withdrawals from the ports in China over the last two weeks. One way to look at this is that the sellers are removing their inventories to clear up space for more ore in transit. Alternatively, it could also imply that ore buyers are getting skittish and have started buying following improving sentiment (i.e. a hike in finished steel spot and futures prices on week 29).

A dominant share of Mn ore stocks inland and onboard in transit to China were acquired at a higher cost implying a loss position for the sellers, contributing to rising downside risk and simultaneously weighing down on the baseline Mn market outlook. Furthermore, the looming uncertainty in real estate financing and the lagging effect state’s infrastructure programs in China have on actual steel demand cast additional worries. Consequently, if a major negative price correction results from disappointing demand recovery and the glut of ore available to the market in China, traders will be willing to close their positions at any price to minimise their losses.

if a major negative price correction results from disappointing demand recovery and the glut of ore available to the market in China, traders will be willing to close their positions at any price to minimise their losses.

LCIB argues that a shortfall in Indian imports is not likely to last, despite Indian buyers and spot resellers sitting on excessive stocks. We assume that a seasonal rebound in domestic demand in China will keep a lid on the country’s steel export sales, allowing Indian steel traders some room for manoeuvre in Asia and thus supporting Mn consumption in their home country. Furthermore, Indian Mn ore buyers tend to resort to accumulating Mn ore at low price levels. It allows us to expect the procurement to restart in the near term and at short notice, although possibly at the lower levels.

In general, the supply cycle of the spot market and the direct procurements pattern in China have changed dramatically in 2022. S32 Australian high-grade ore export delinquencies complemented the irregular pattern of Eramet shipments, translating into higher selling power held by both companies. The new supply paradigm requires the low-grade SAR producers to adjust to the new realities, not to mention to resort to supply discipline in one way or another in the meantime, especially in light of boisterous growth in Eramet’s exports.

As of now, the Chinese buyers have adopted a wait-and-see stance, while Europe and Russia, in particular, are absorbing volumes lost in India, although that is not going to last with sellers turning to China eventually. Hopefully, the demand recovery will be there to underpin the growth in the manganese market.

We would be happy to answer your question or discuss LCIB manganese reports. To reach out, please email us at: manganese@londoncib.com

LCIB Manganese Team

{kind=link}

{kind=link}

{kind=link}