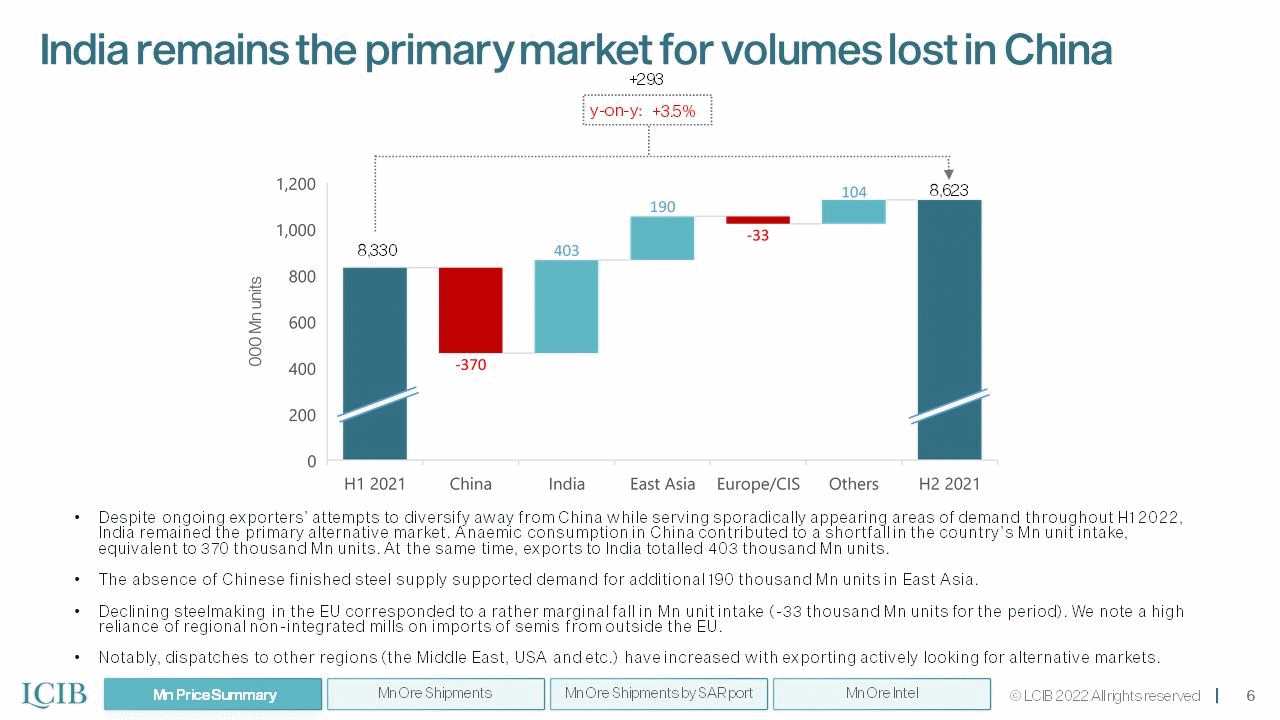

During H1 2022, India became the fastest-growing Mn Ore regional market

Lithium prices decoupling from demand fundamentals intensifies

21 April 2022

Impact of Collapsing Shipments to India on Manganese Market Outlook

28 July 2022

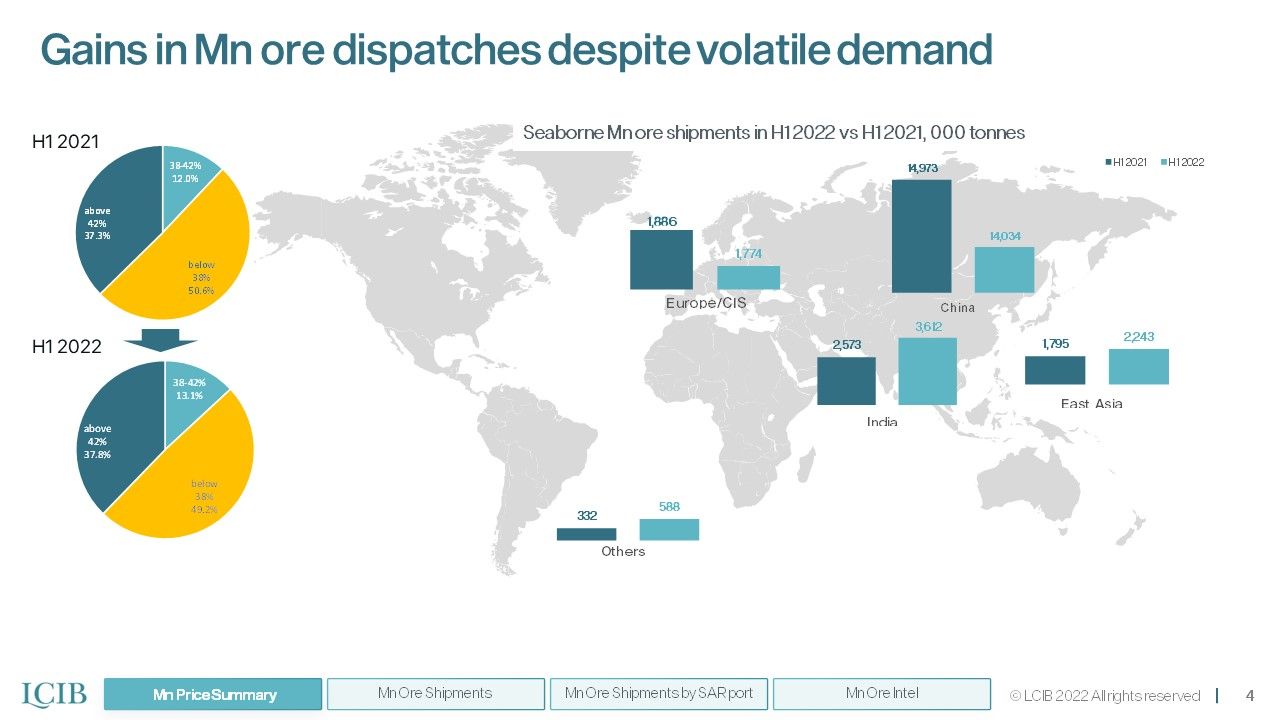

Despite the ongoing slump in global steelmaking, the H1 2022 actual Mn ore dispatches have demonstrated growth on y-on-y in nominal terms and Mn units dispatched. The total volume shipped during the first half of 2022 totalled 22.31 million tonnes and was +7.3% y-on-y higher than H1 2021 dispatches. Similarly, dispatches of Mn units grew +7.5% y-on-y. Global dispatches were fuelled by bolstered Mn ore exports ex-SAR, Gabon and Ghana. At the same time, Australian dispatches decline amid lower S32 and the absence of OMH exports to China.

A destabilisation of the global macroeconomic resulted in tightened monetary policies by central banks with higher lending rates strengthening the USD exchange rate. Slowing economic growth concerns, spiking inflationary pressure, and the resulting volatility further dampened growth projections. Moreover, the unresolved issues along the global supply chains prone to exacerbated commodity prices contributed to further propagation of inflation already underpinned by escalating political risks. In China, finished steel consumption was severely curbed by extensive covid-19 lockdowns. The start of the military conflict in Ukraine not only affected the global flows of finished steel and Mn alloys but indirectly contributed to a slowdown of steelmaking in the EU amid a looming energy crisis resulting from spiking natural gas prices. Indian steel and Mn alloy producers took over the niche aiming to replace a shortfall in finished steel and alloy supply. Yet, introducing an export tax for finished steel in the country allowed the Middle East and East Asian steelmakers to tap into unmet demand. A reopening of China allowed Chinese commodity-grade material to become the dominant source of finished steel in late Q2. Yet, a disappointing domestic industrial demand forced a rapid downscaling of the crude steelmaking in the country in June. Such chaotic Mn demand developments contributed to increasing geographic diversification of Mn ore sales. Yet, the market participants seemingly fail to react to the changes at the speed these changes appear, with a surge in sales to India in late June while compensating for slowing Chinese steelmaking seeming counterintuitive in the current market circumstances.

A rapid growth in Eramet dispatches during the first half of 2022 led to marginal gains in high-grade ore shipments, effectively mitigating falling S32 exports. The low and mid-grade ore dispatches have started to decline since May, though.

During H1 2022 Indian market managed to absorb Mn ore volumes lost in China.

{kind=link}

{kind=link}

{kind=link}